Integrated Thinking

A company report is both a duty and an opportunity. About one third of German companies are obliged by law to publish their annual accounts. Since 2018, capital market-oriented companies of a certain size are also obliged to report on non-financial aspects such as their contributions to environmental and climate protection. This might seem like a heavy burden at first sight. Yet, reporting on social responsibility offers a company a whole range of opportunities to profile itself in all its manifold aspects to make itself interesting for investors and other stakeholders. So it is not entirely due to statutory prescriptions, if for the past few years company reporting has been in a process of change. Financial reporting, which is mainly geared to the past, is increasingly being paired with forms of much more forward-looking reporting such as sustainability reports and integrated reports.

Integrated reporting follows the goal of intermeshing a variety of reporting instruments. Ideally, a number of stand-alone financial and sustainability reports are aggregated to produce a corporate report that articulates key aspects of value creation. The framework of the International Integrated Reporting Council (IIRC), for instance, gives a set of recommendations on how to compile an integrated report. It proposes that an integrated report should put its focus on the company’s business model and describe the interrelations between economic, social, environmental, and governance-related aspects of the company. The point of the exercise is to give a clear image of how the company creates value in the short, medium, and long-term perspective.

Erfolgsfaktoren mit Benchmarking feststellen.

Integrated Thinking made by Fraunhofer IPK

Integrated reporting should also serve to turn the company’s internal management perspective more to the outside in order to give external stakeholders a more comprehensive view of the company. In this context, it seems only logical to go a step further and use integrated reporting as a strategic management tool internally. In line with the saying »the journey is the destination«, the very process of compiling an integrated report can in itself serve to promote integrated thinking. The goal of integrated thinking, in turn, is to completely break with the isolated consideration of individual topics or fields of interest (»silo thinking«). What it proposes instead is to start with a company's business model and present the financial and non-financial impacts of company activities and the ways in which they are interconnected.

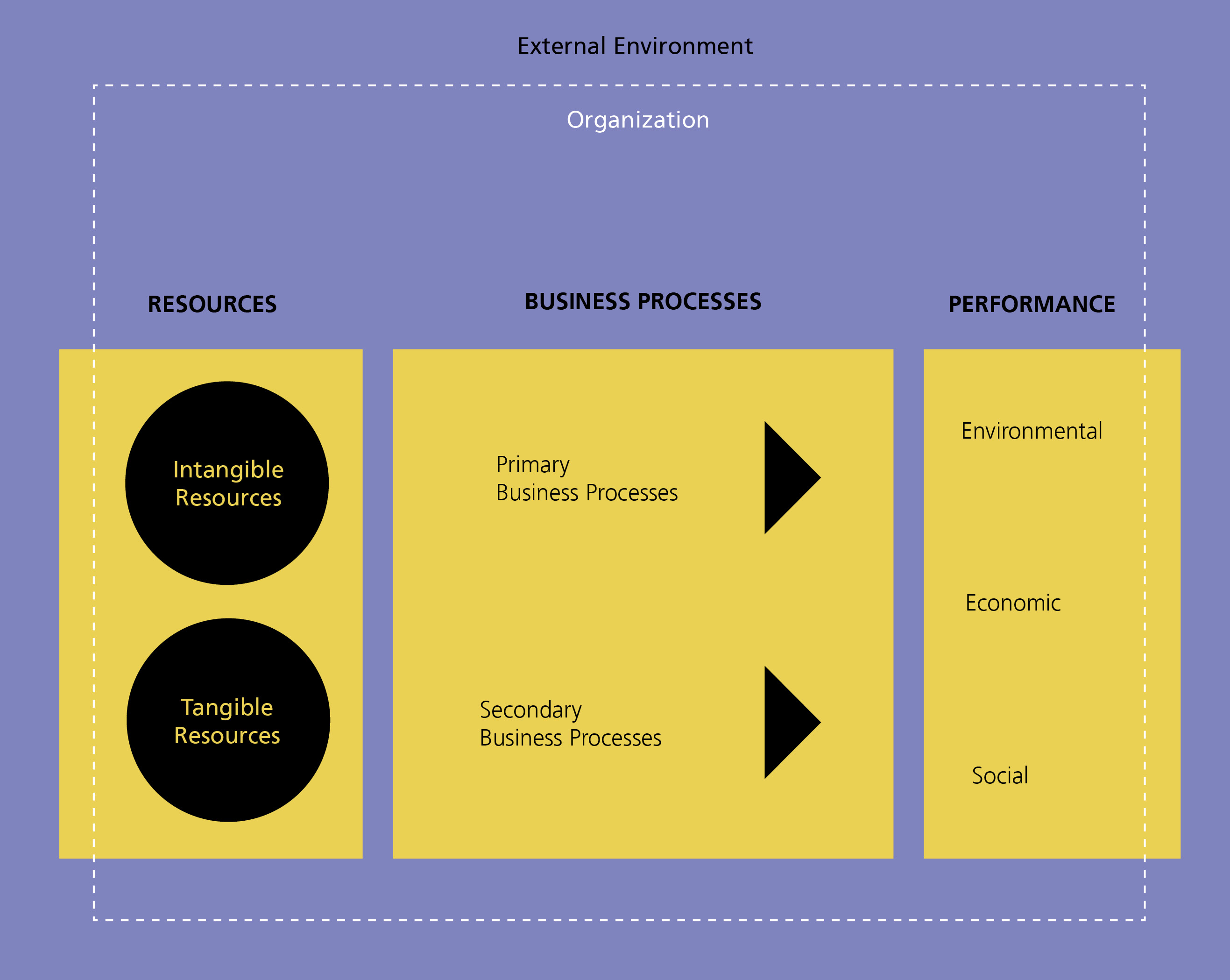

Fraunhofer IPK drives the idea of integrated thinking to the extremes: From the very outset, all relevant aspects of the company are embedded in a company model from which ultimately not only reports can be derived. This reference model can map out any company in its full individuality. It is rooted in the basic assumption that not only judicious use of tangible resources (e.g. raw materials, energy, machines) are key factors in ensuring the success of sustainable company development. Intangible resources (e.g. the knowledge, skills and abilities of its workforce, a motivational company culture, stakeholder relationships) are least as important in ensuring this goal. All of these aspects form part of the reference model.

Fraunhofer IPK also endows the model with a range of coordinated instruments and procedures for analysis, planning, control and reporting in the company. These include a self-assessment procedure, a key figure catalogue and a reporting system for the analysis and control of operational processes, resource bases and sustainability performance.

The Fraunhofer reference model for shaping sustainable corporate development provides the basic structure for the Integrated Sustainability Cockpit.

The Sustainability Cockpit

The key tool in the Fraunhofer IPK solution is the integrated Sustainability Cockpit (INC), which embeds sustainability aspects in conventional management systems. The system takes advantage of the fact that digital analysis and visualization technologies play a major role in supporting corporate decision-making today. A controlling and reporting system was evolved that draws on instruments from the field of business analytics. The tool systemizes the process of information gathering and analysis through to decision making. Thus, it not only supports integrated reporting, but above all promotes integrated thinking within the company.

Thanks to various interaction opportunities, users enjoy wide-ranging options to freely design their own analysis paths. The cockpit supports monitoring of key indicators and can be used to identify problems, track measures or for supervision of successful strategy implementation. Decision-makers can gain a better understanding of opportunities and risks, assess alternative decisions, and dialogue with one another across the whole company. What is more, the content of the cockpit can be used as a basis for both internal and external communication activities.

Advantages of Digital Reporting

Digitalization enables us to break with traditional print and PDF formats and open ourselves to interactive formats of reporting. Unlike print reports, which give a snapshot of sustainability-related information, digital reports can be continually updated. Extensive detailed information can be prepared for particular target groups.

Search and filter mechanisms allow users to rapidly search for and retrieve essential content. Moreover, digital reporting facilitates cross-references between the contents of reporting. Interdependencies can be presented in a clear and understandable manner. Interactive data analysis and visualization of a range of diagrams, portfolios and tables also enhance the communicative quality of the digital report.

Artificial Intelligence and Reporting

Artificial intelligence (AI) is steadily gaining in importance in both research and industry. Experts agree that artificial intelligence and machine learning will have a massive influence on company reporting. AI applications could be useful in the evaluation and visualization of data by pointing out important casaulities and optimizing repetitive processes like quality control. In the near future, new universal reporting standards will support automatic analysis regardless of language, company and industry sector.

Even so, AI-based reporting systems bring their own challenges, as they require a profound understanding of the data situation. Companies will have to build the skill sets needed. Experts agree that technology alone is not enough – solid background knowledge is still an essential.